March 2017 Market Summary Report for Central Texas; including Austin area, Travis, Williamson, and Hays Counties:

|

|

|

|

|

|

||||||

|

||||||

March 2017 Market Summary Report for Central Texas; including Austin area, Travis, Williamson, and Hays Counties:

|

|

|

|

|

|

||||||

|

||||||

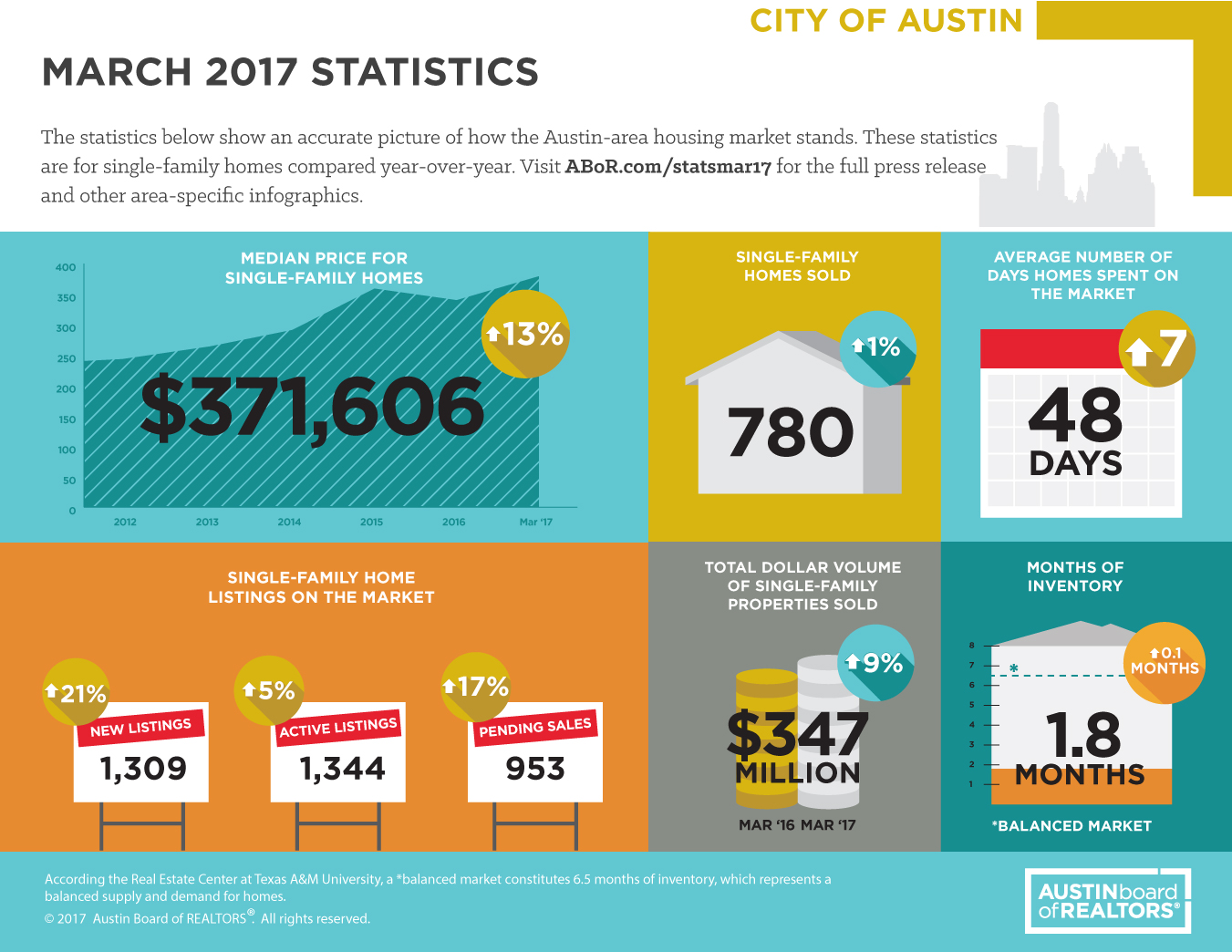

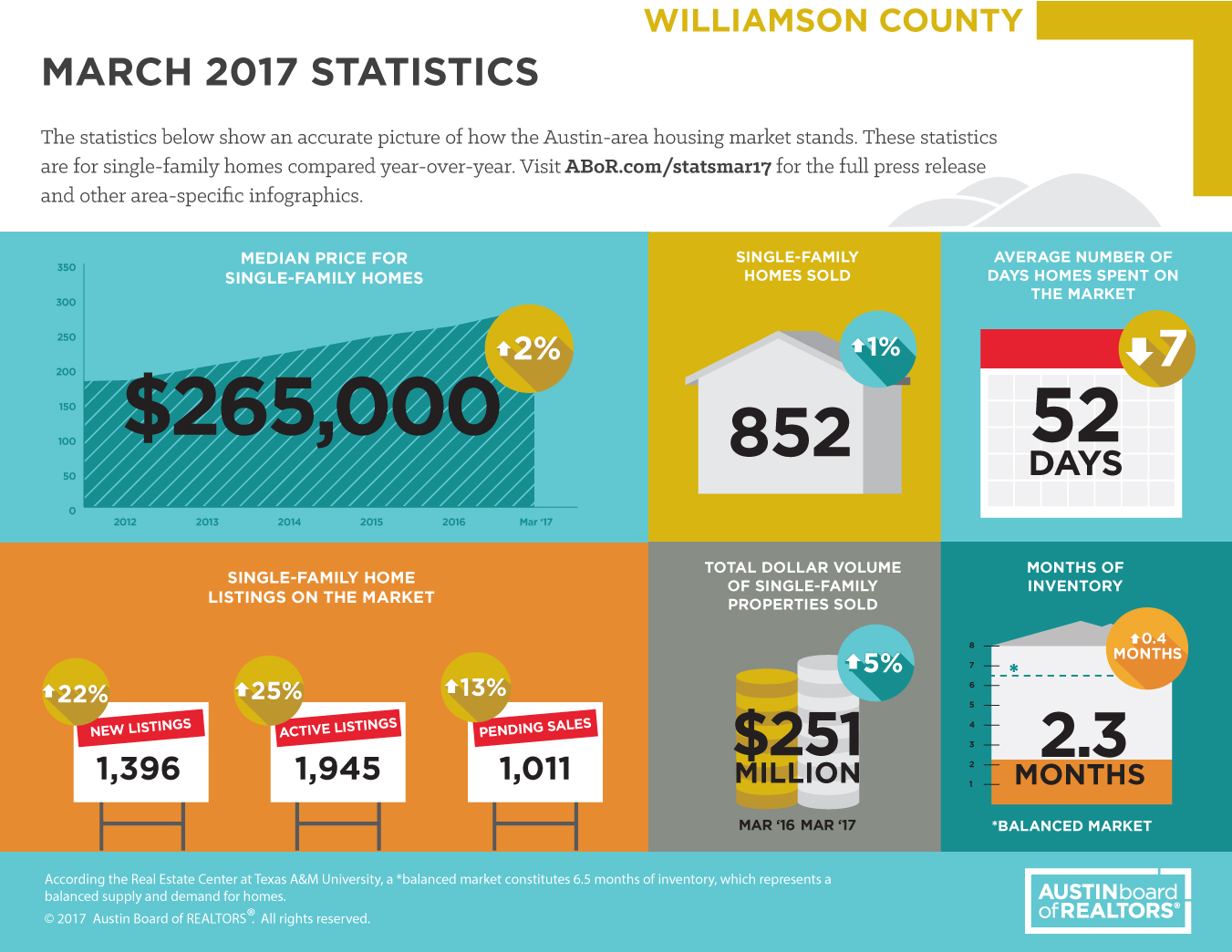

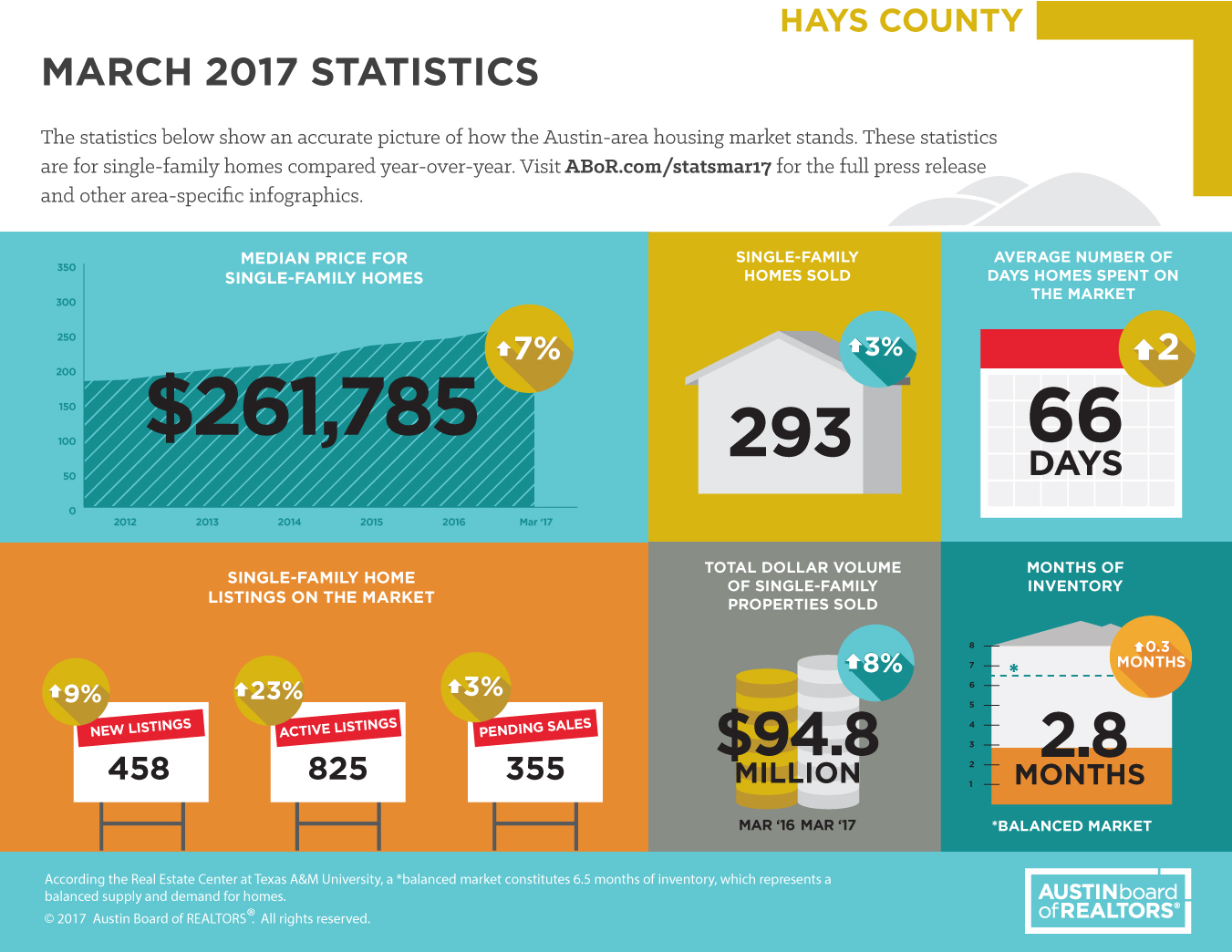

In a March 16, 2017 press release, the president of the the Austin Board of REALTORS® described the signs of slow home sales as “the market catching up to itself after years of unprecedented sales growth”. He further explained that current figures are compared to a very strong housing market activity in 2016, so a decline in home sales growth is understandable and does not automatically mean that “the market is softening.”

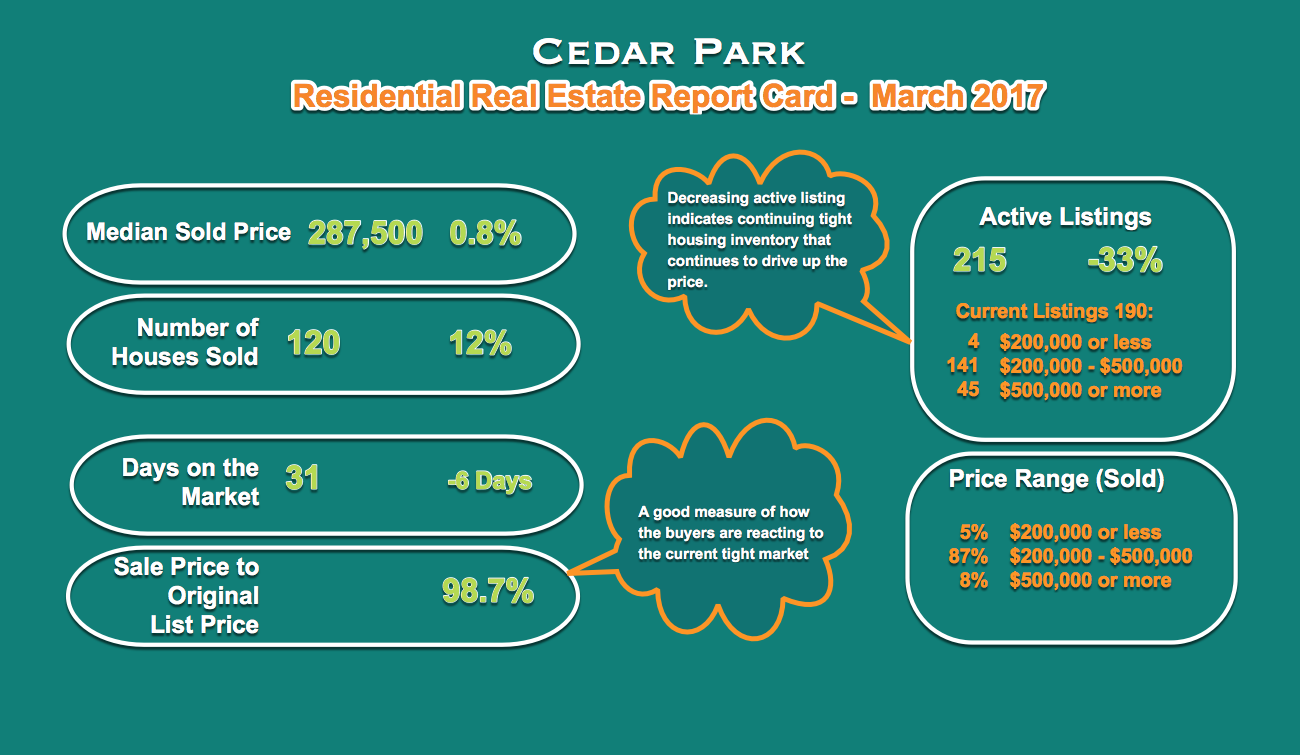

If you follow these monthly reports, you may have noticed a similar trend in the Cedar Park housing market in recent months. For the second consecutive month the median price of the houses sold remains flat. However, as another metrics (below) indicates, a decrease in the active listings and a lower inventory of available houses for sale points to a high demand and a strong market.

I have started to report a new metrics for “Sale Price to Original Asking Price” ratio in the report card. This measures how close to the asking price a house is sold. It is a good indicator for the level of demands and how ‘hot’ the market may be.

In case your are considering a move in the coming months, start with bringing your house up to date. Get an inventory of needed repairs and bring your house in tip-to shape for maximum sales value. Whether you are refinancing or buying a new house, take into account all the the selling (closing) costs. Like any other business decision, knowledge is key in a successful real estate transactions. Find out how you can sell your house at the right price. Get an estimate of the closing costs and who pays them, and contact a knowledgeable agent for consultation.

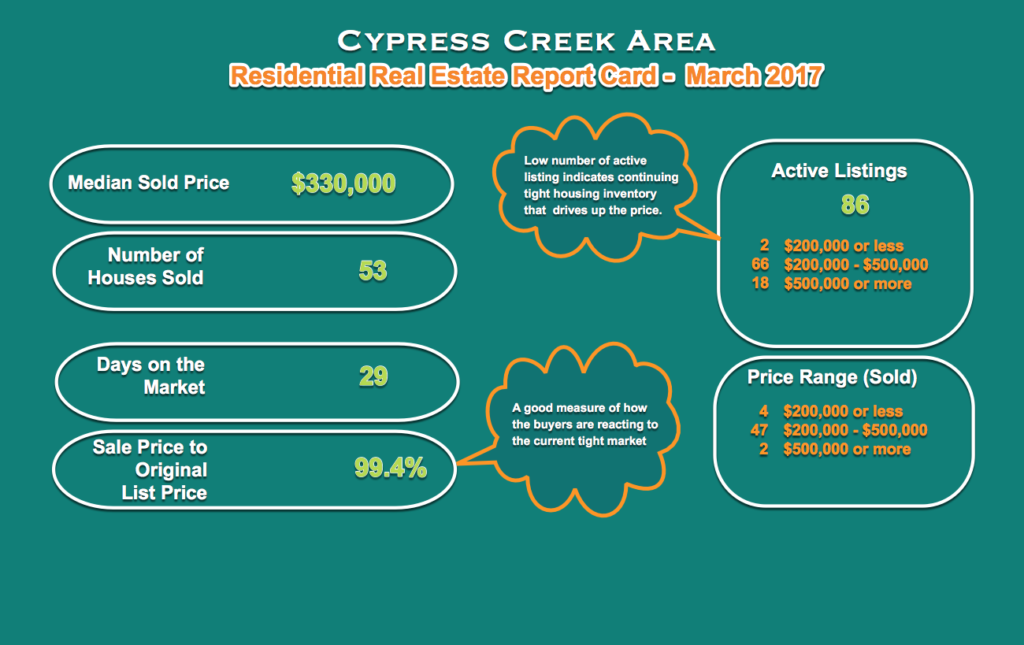

You can explore details (click on the marker for details of each sale) of all the 53 Cypress Creek Area home sales during March 2017 in the interactive map below.

For the city of Cedar Park single-family home sales during March is summarized below. All comparisons are relative to March 2016.

All this activity has affected your home’s value!

If you plan to move, you need to know the value of your home right now. You can find this out in two easy ways:

I hope you find this helpful. Referral is a big part of my business and as always I appreciate your consideration in referring any friends, family, or colleagues my way. Thank you for supporting me and my business endeavors. Please don’t hesitate to ask me questions about real estate, your desired neighborhoods, or your house value!

Best wishes,

|

||||||

|

||||||

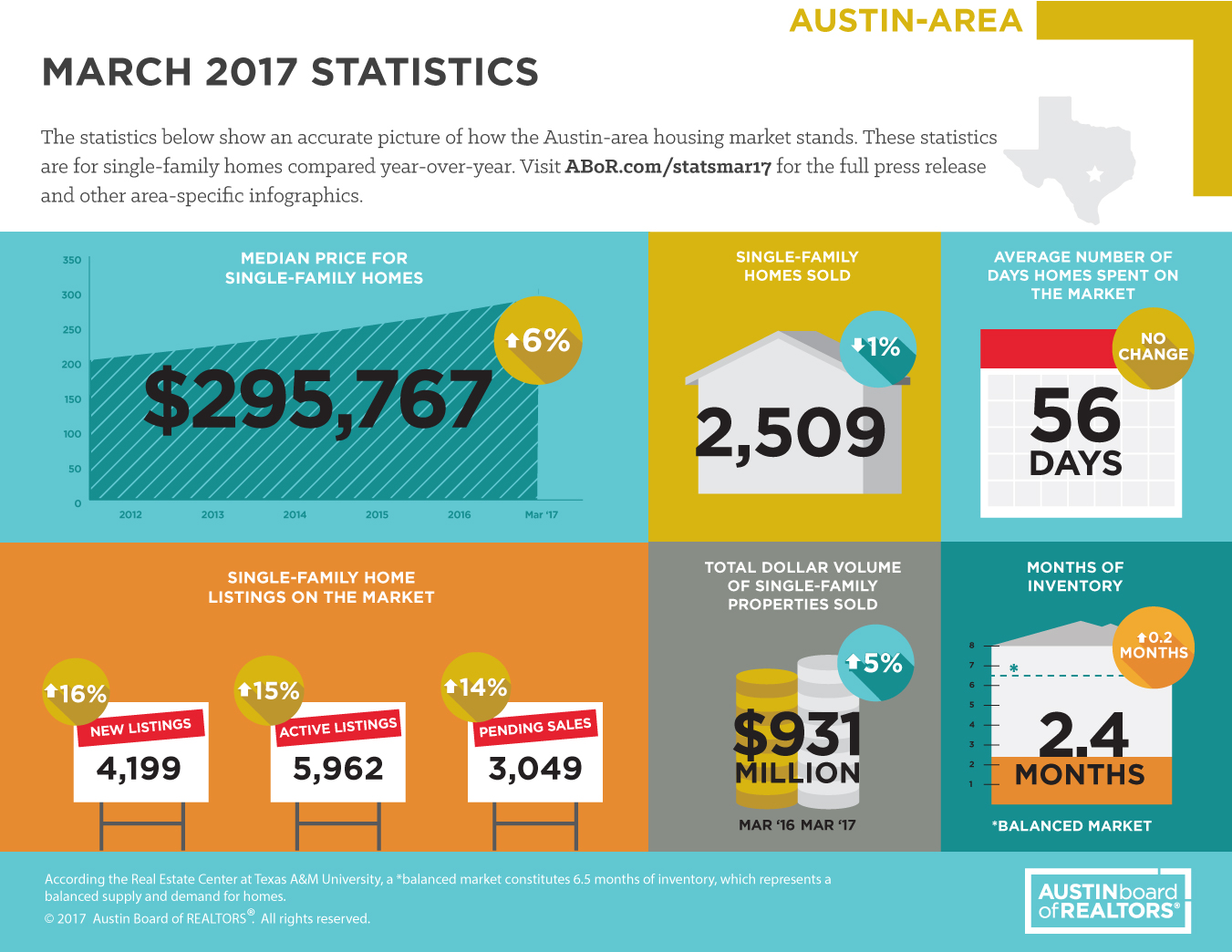

In a March 16, 2017 press release, the president of the the Austin Board of REALTORS® described the signs of slow home sales as “the market catching up to itself after years of unprecedented sales growth”. He further explained that current figures are compared to a very strong housing market activity in 2016, so a decline in home sales growth is understandable and does not automatically mean that “the market is softening.”

If you follow these monthly reports, you may have noticed a similar trend in the Cedar Park housing market in recent months. For the second consecutive month the median price of the houses sold remains flat. However, as another metrics (below) indicates, a decrease in the active listings and a lower inventory of available houses for sale points to a high demand and a strong market.

I have started to report a new metrics for “Sale Price to Original Asking Price” ratio in the report card. This measures how close to the asking price a house is sold. It is a good indicator for the level of demands and how ‘hot’ the market may be.

In case your are considering a move in the coming months, start with bringing your house up to date. Get an inventory of needed repairs and bring your house in tip-to shape for maximum sales value. Whether you are refinancing or buying a new house, take into account all the the selling (closing) costs. Like any other business decision, knowledge is key in a successful real estate transactions. Find out how you can sell your house at the right price. Get an estimate of the closing costs and who pays them, and contact a knowledgeable agent for consultation.

The Cedar Park single-family home sales during March is summarized below. All comparisons are relative to March 2016.

You can explore details (click on the marker for details of each sale) of all the 120 Cedar Park home sales during March 2017 in the interactive map below.

All this activity has affected your home’s value!

If you plan to move, you need to know the value of your home right now. You can find this out in two easy ways:

I hope you find this helpful. Referral is a big part of my business and as always I appreciate your consideration in referring any friends, family, or colleagues my way. Thank you for supporting me and my business endeavors. Please don’t hesitate to ask me questions about real estate, your desired neighborhoods, or your house value!

Best wishes,

|

||||||

|

||||||

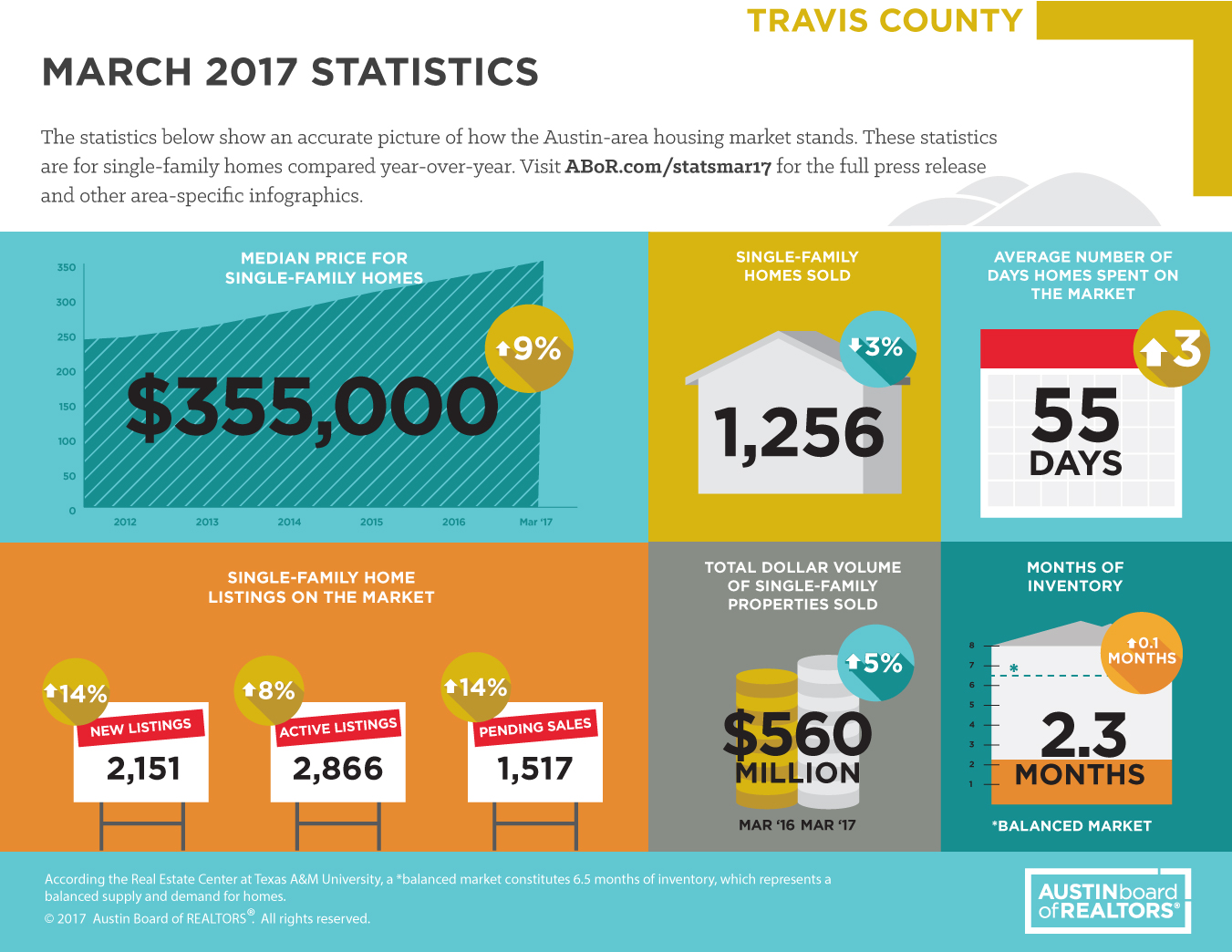

In a March 16, 2017 press release, the president of the the Austin Board of REALTORS® described the signs of slow home sales as “the market catching up to itself after years of unprecedented sales growth”. He further explained that current figures are compared to a very strong housing market activity in 2016, so a decline in home sales growth is understandable and does not automatically mean that “the market is softening.”

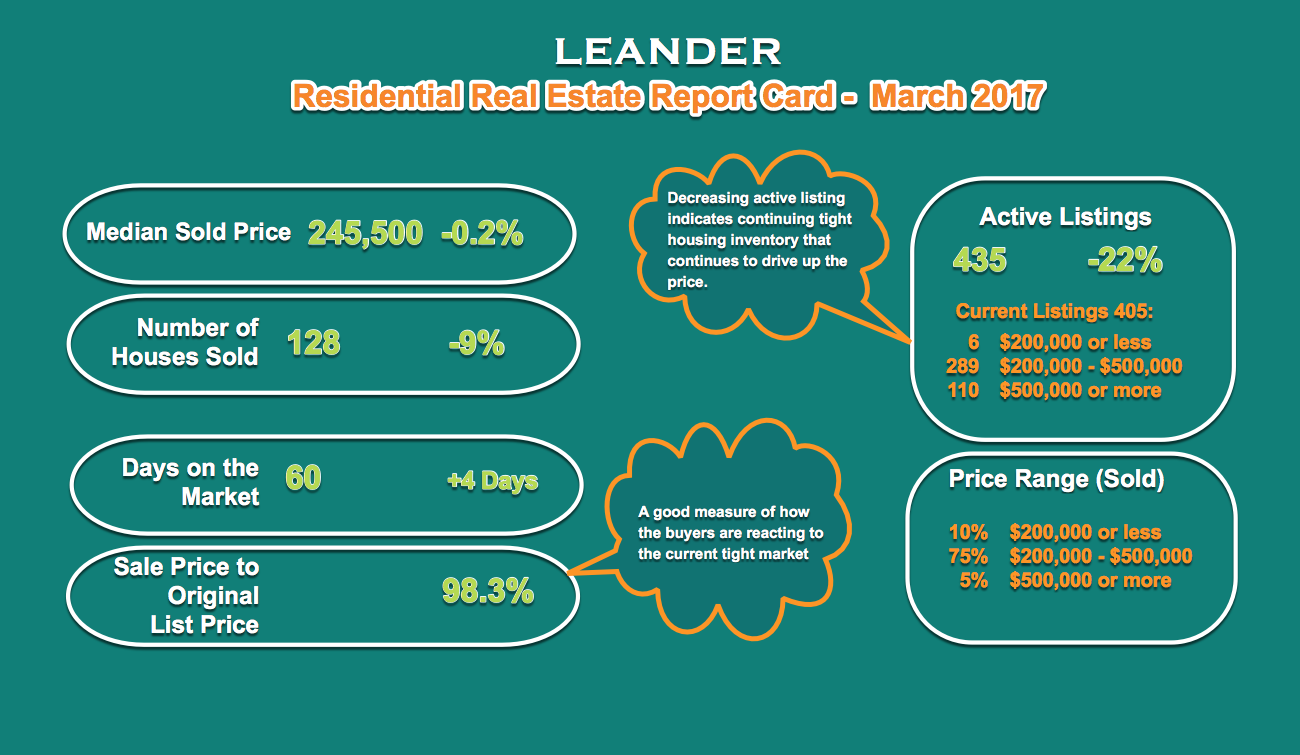

If you follow these monthly reports, you may have noticed a similar trend in the Leander housing market in recent months. For the second consecutive month the median price of the houses sold remains flat. However, as another metrics (below) indicates, a decrease in the active listings and a lower inventory of available houses for sale points to a high demand and a strong market.

I have started to report a new metrics for “Sale Price to Original Asking Price” ratio in the report card. This measures how close to the asking price a house is sold. It is a good indicator for the level of demands and how ‘hot’ the market may be.

In case your are considering a move in the coming months, start with bringing your house up to date. Get an inventory of needed repairs and bring your house in tip-to shape for maximum sales value. Whether you are refinancing or buying a new house, take into account all the the selling (closing) costs. Like any other business decision, knowledge is key in a successful real estate transactions. Find out how you can sell your house at the right price. Get an estimate of the closing costs and who pays them, and contact a knowledgeable agent for consultation.

The Leander single-family home sales during March is summarized below. All comparisons are relative to March 2016.

You can explore details (click on the marker for details of each sale) of all the 128 Leander home sales during March 2017 in the interactive map below.

All this activity has affected your home’s value!

If you plan to move, you need to know the value of your home right now. You can find this out in two easy ways:

I hope you find this helpful. Referral is a big part of my business and as always I appreciate your consideration in referring any friends, family, or colleagues my way. Thank you for supporting me and my business endeavors. Please don’t hesitate to ask me questions about real estate, your desired neighborhoods, or your house value!

Best wishes,

|

||||||

|

||||||

You have heard it countless time that buying a house is the largest purchase you make in your life. For many, that is absolutely true and for that investment it makes perfect sense to get as much information as possible about the how to buy a house.

Even with prior knowledge and preparation, many first-time home buyers, make a mistake or two along the way. Buying more house than you could afford, or taking on a more decrepit house than you could realistically make habitable, are examples of those mistakes. Despite their best intentions, agents can only do so much with their advice.

The first-time buyers who are happiest are those who had done their research, and planned their purchases, communicated with their partners and agents and did not step too far outside of their comfort zones. A home is often a big part of your lifestyle, so when you find the right house that meets your criteria, be prepared to pull the trigger and follow through. Waiting to get absolute best possible deal may not be the best strategy. Creeping interest rates and lost opportunities could eat up any saving in the deal.

Financing is one of the major obstacle in most home buyers decision making process. Even though affordable housing is out of reach for lots of people, there are still programs to help people in their home ownership dreams. If you live in Travis Country, I would like to introduce two such programs.

My First Texas Home Program

This program allows qualified Texans access to low interest rate home loans, and help with down payment and closing cost assistance. The benefit is simple, you get more house for the same down payment or qualify for house easier. You can begin a lifetime of homeownership through My First Texas Home.

Homebuyers who meet the following minimum requirements are eligible to apply for a loan under the program:

To verify eligibility and apply for these loans, take your personal financial information to your lender. At the time of loan application, you will need the following:

Texas Mortgage Credit Certificate (MCC) Program

This program hat increases a family’s disposable income by reducing its federal income tax obligation. This tax savings provide a family with more available income to qualify for a loan and meet mortgage payment requirements. It is available to teachers, fire fighters, peace officers, veterans, and low and moderate-income homebuyers. This program is available through a network of lenders across the state and provides the following benefits:

The example below assumes a family purchases a home for $200,000 at a 4.75% interest rate. Interest paid the first year is approximately $9,500. The 40% of the interest paid would equal $3,800 (40% x $9,500 = $3,800).

| Mortgage Amount | $250,000 |

| Interest Amount | 4.75% |

| Interest Paid | $9,500 |

| MCC Rate | 40% |

| Tax Credit | $2,000 |

In this example, the homebuyer would be entitled to a tax credit of the maximum $2,000.00. It is important to note that the homebuyer will still be able to take a mortgage interest deduction

So the question if affordability should be, have your explored all available options to make the home buying easier on your pocket? Let’s get started!

Best wishes,

|

||||||

|

||||||

Like everything else in a real estate transaction, closing costs (costs associated with buying or selling a property) are negotiable. Part of the closing costs, such as title insurance, regulated by the state of Texas and is based on a predetermined formula. Others costs are such as association fees, realtor commissions, etc. are negotiable and depend on the price of the house.

Buyer can request the seller to cover some or all of the closing fees. One way is to offer the full purchase price provided that the seller pays all the costs associated with closing. Most sellers expect homebuyers to offer less than the listing price, so they are much more open to negotiate when they have a full price offer at hand. Another option is for the buyer to meet the seller halfway, dividing the closing costs between the two parties.

Regardless of who ends up paying the closing costs, the following steps help making an informed decision.

|

||||||

|

||||||

In a typical real estate transaction in state of Texas, there are many charges that are paid at the closings. Most, if not all, of these charges are negotiable. Here is a list of some estimated costs.

| Charge | Description | Amount | Who Pays |

| Appraisal | The appraisal is required to determine the fair market value of the home. A property appraisal is generally required by a lender before loan approval to ensure that the mortgage loan amount is not more than the value of the property. Therefore, an appraiser is needed to make this determination. | $300-400 | Buyer |

| Courier/FedEx | At times, documents need to be shipped to other places. This can be for the buyer or the seller and it is charged to the benefiting party. Not commonly negotiated in the formal contract for sale, your closing agent will collect these charges at closing. | ~$50 | Buyer, Seller |

| Document Preparation | Covers the cost of preparing the final legal papers, such as a mortgage, deed of trust, note or deed. | ~$125 | Buyer |

| Escrow Fee | Fee for title company’s services in receiving and holding funds (earnest money, buyer purchase money funds, loan funds, etc.) and disbursing those funds to the various parties. This requires a separate accounting for each transaction. All funds must be received, and the account must be balanced before any checks are sent cut. | ~$200 | Buyer, Seller |

| Home Warranty | $Fee for an insurance policy to protect you from cost of unexpected failures in the major systems and appliances of your new home. | ~$500 | Buyer |

| HOA Resale Certificate | Some neighborhood Home Owner Associations require a transfer fee at the time of home sale. | $500-$700 | Negotiable |

| Mortgage Insurance Premium | The lender may require you to pay your first year’s mortgage insurance premium or a lump sum premium that covers the life of the loan, in advance, at the settlement | Varies | Buyer |

| Prepaid interest | This is money you pay at closing in order to get the loan interest paid up through the first of the month. | Varies | Buyer |

| Property taxes | The property taxes for the balance of the year from the closing date. This is collected from buyers and seller pays for the previous months, so the title company can pay the first ear’s property taxes. | Depends on closing date | Buyer |

| Realtor Commission | Generally the seller is represented by an agent. This fee is negotiated by the listing agent and seller when the property was listed for sale. A portion of this fee is offered to the other agent (buyers agent) . There is no law requiring this co-brokerage arrangement and sometimes listing agents are unwilling to share their commission with a selling agent. In this case, unless the buyer expects his agent to work for free, both seller and buyer may pay a brokerage fee. This fee is almost always paid at closing, except on some owner-financed deals. | Depends on the loan amount | Seller |

| Recording Fees | These are the fees that the county charges for recording the new deed and mortgage into the public record. These are sometimes referred to as Deed or Mortgage taxes and is based on the sales price of the property, the number of pages, number of documents, and when recording mortgages, the value of the mortgage. In cash transactions, sometimes it is left up to the buyer to physically carry the deed to the recording authority after the closing. This is a negotiable cost but realize the seller has no interest in whether or not a buyer’s documents get recorded. Thus the buyer usually pays the fees and is calculated for each page of documents to be recorded (e.g. $26 for the first page and $4 for each additional page). | ~$15 | Buyer |

| Survey | The lender may require a property survey. This is a protection to the buyer as well. Unless there is a very recent survey, it is a advised to get a survey done that corresponds with the physical boundary lines that are evident on the property. Having a current, clear survey is one of the best sales tools a seller can have. This is one that you just work out by negotiation. Care should be taken as to what type of survey you are negotiating. It could be as simple as having the corners marked, and a legal description derived from the information gathered in the field and previous deeds. It could also include fences, roads, and structures located on the plat of the property, boundary lines marked. Sometimes it may be necessary to include a topographical survey as well. | ~$400 | Buyer / Negotiable |

| Title Policy –Lender | When a lender agrees to issue a mortgage for a piece of property, the lender must receive a guarantee that the property is indeed owned by the seller. Title fees pay the lender for the costs associated with determining the current owner of the property and legally certifying that the title information is correct.

In addition to the formal title search, your lender is likely to require a title insurance policy to protect it against an error in the title search. Errors are rare, but they do occur. Premiums and the scope of coverage can vary widely. As a rule, look for a policy with the least exclusions from coverage as possible. The title insurance required by the lender protects only the lender. To protect yourself against unforeseen title problems, you may also want to take out an owner’s title insurance policy. Normally the additional premium cost is only a fraction of the lender’s policy. |

Depends on the loan amount

~$1800 for $250K |

Buyer |

| Title Policy –Owner | The owner’s policy protects the homeowner’s investment for as long as they, or their heirs, own the property. This fee charged by the title company to search public records to determine if there are any title issues such as breaks in the chain of title, any unsatisfied mortgages, liens or judgments which have been recorded.

When it comes to houses, providing clear title is not a simple process. Public records affecting real estate title are spread among several local government offices, including recorders of deeds, county courts, tax assessors, and surveyors. Records of deaths, divorces, court judgments, liens, and contests over wills also must be examined. Examinations also review the history of ownership, including all trusts, will and deeds associated with the property in the past. This is called reviewing the chain of the title, and inspects whether the property’s ownership may be legally tied to anyone other than the current buyer and seller. |

Depends on the sale price of the house

~$1800 for $250K |

Seller |

|

||||||

|

||||||